Anil Thakersee, Executive: Marketing & Business Development

Investing offshore is an important part of any long-term investment strategy, as it offers diversification beyond the opportunity set available via South African markets.

South Africa is a relatively small, open economy with around 330 investable companies listed on the local exchange with a market capitalisation of just over US$1 trillion. To put this into context, total global equity markets had a market capitalisation of just over US$94 trillion in the same period. In essence, the South African market represents around 1% of global equity markets.

In addition to the wide breadth of industries and companies available in global markets, the additional benefit is exposure to economic growth in foreign economies, which makes your portfolio less dependent on growth in the South African economy to drive overall returns.

Investing offshore remains an important tool in the asset class toolbox to build diversified portfolios. The blending of different asset classes, each occupying different coordinates on the risk-return spectrum, optimises the overall risk-return profile at a total portfolio level.

Forecasting the rand

The rand is not just the metric most South Africans use to measure their financial wealth but is often seen as a reflection of our country’s share price. As a result, fluctuations in the local currency can impact investor sentiment and at times trigger reactive decision-making. It is worth noting that the wild swings seen in the currency over the last few decades have almost all been related to global events resulting in declining global risk appetite and declining global liquidity. This is not to say we don’t have social and growth challenges as an economy, however, is a system of floating exchange rates the equation is more dynamic and we have a multitude of factors impacting the exchange rate.

As one of the most liquid emerging market currencies in the world, the rand, at times, can indeed be very volatile. Several things tend to impact the rand, including commodity prices, inflation differentials, interest rates, economic growth and the impact of domestic issues. This makes it exceedingly difficult to try and predict where the rand is going to end up over the short term.

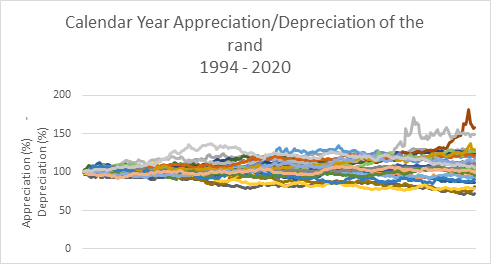

Figure 1 shows the calendar year appreciation or depreciation of the rand over 26 years, with each line representing an individual year. From year to year, it doesn’t have a discernable pattern and, for the most part, trying to determine the movement of the rand over the short term is very much a guessing game.

Figure 01

Source: IRESS

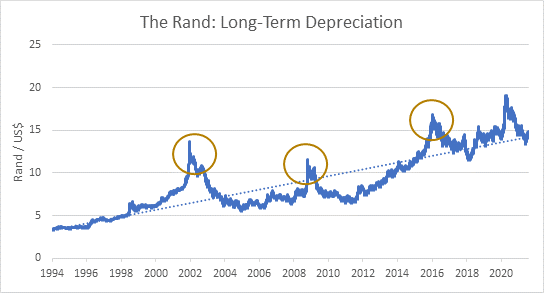

Historically, the rand tends to depreciate over the long term. The circled points in Figure 2 highlight periods of heightened uncertainty in markets where the rand tends to overshoot in weakness, however, the trend since 1994 has been for the rand to depreciate. However, it is worth noting that while this depreciation has been in nominal terms, in real terms (after factoring in inflation differentials) the rand remains close to its Purchasing Power Parity (shown by the dotted line) which accounts for the inflation differential. Countries with higher rates of inflation, like South Africa, will have their currency depreciate against a country with lower inflation.

Figure 2

Source: IRESS

80 Years of sharing success

R27.7BN total cumulative profit-share allocation to members with qualifying products over the last 10 years.

Offshore investing – navigating a world of investment opportunities

A major theme playing out in recent years has been the strong outperformance of growth stocks over value stocks and to some degree, this has been a driving factor in performance for global portfolio managers.

The top 10 companies of the S&P 500 account for nearly a quarter of the total market capitalisation of the index. These giants have, in recent years, done the heavy lifting for the index and exposure, or lack of exposure, to these companies, has skewed investment performance.

In addition, global managers have had to balance exposure to structurally faster growing emerging markets against more stable but lower growth developed markets. This has been made even more challenging in the pandemic environment where different countries are in different phases of re-opening their economies.

Once the decision has been made to allocate to offshore-based assets, there are numerous challenges in identifying and selecting the best partners. At PPS Investments, our focus has been to partner with large established managers who have a long track record of consistently delivering excess returns through the various cycles and volatility presented by markets.

Sound financial planning advice remains critical for clients when structuring investments to meet their required outcomes and this includes balancing domestic and offshore investments.