John Anderson, Executive: Investments, Products and Enablement, Alexforbes

In his budget speech on 22 February 2023, the Minister of Finance announced that the proposed two-pot system will take effect on 1 March 2024.

Many had hoped for a delayed implementation date, given the development required to systems to accommodate the new structure.

The proposed amendments will allow short-term access for South Africans to their retirement fund money for emergencies within set limitations, while balancing this access with long-term preservation of savings for retirement. To effect the relevant changes, the Income Tax Act will include the following new definitions for “savings pot”, “retirement pot” and “vested pot”.

An important aspect mentioned is that some immediate access to retirement savings accumulated to 1 March 2024 could be accessed. This follows consultation and is a departure from previous comments which would not allow immediate access of past contributions.

It is expected that more detailed legislation would be released in due course, specifically dealing with:

(i) “Seed capital”, allowing individuals to have a starting balance in their “savings pot” which would be accessible at any time

(ii) The treatment of defined benefit funds

(iii) The treatment of “legacy” retirement annuity funds

Another aspect to be dealt with in a second phase of implementation, is allowing individuals who are retrenched and have no alternative source of income to be able to access their retirement pot.

What is the proposed two-pot system?

This system aims to find the right balance to help members save for retirement while allowing some flexibility for short-term emergencies. The ‘two-pot’ proposal splits new contributions from the proposed implementation date into two pots of money. For example, let’s say you are a member who has a pensionable salary of R10 000 a month and the contribution rate is 15% (R1 500 per month):

- The first pot is for longer-term financial security – the retirement pot.

R1 000 a month, less any fees and group insurance premiums, will go into the retirement pot (two-thirds). It must be invested until retirement and used to buy a pension from a registered insurer, unless you have saved less than the minimum required amount. The current minimum amount for purchasing an annuity (de minimus R165 000) will apply to the retirement pot. This will improve retirement outcomes for most fund members.

- The second pot is for short-term financial relief – the savings pot

R500 a month, less any fees and group insurance premiums will go into the savings pot (one-third). You may withdraw money from the savings pot once a year at most while working. The minimum amount will be R2 000 per annum. If you withdraw all the savings in this pot before retirement, then you won’t have any money to withdraw from this pot at retirement.

Accessing the savings pot should be as a last resort, particularly as any savings withdrawn from a retirement fund reduces your income at retirement. In addition, if you have used up all the savings in the savings pot, you will not be able to access any cash at retirement from the retirement pot. Generally, it is advisable for you to make use of other savings vehicles for day-to-day savings or to finance non-retirement savings goals.

You know your industry best.

Choose an insurance partner that does too.

Insure your business with Bryte. Visit bryteinsure/co.za or contact your broker.

Bryte Insurance Company Limited is a licensed insurer and an authorised FSP (17703)

Alexforbes’ view

For a long time, we have been advocating for improved preservation of retirement savings in South Africa. At present, when an individual leaves employment they can effectively access 100% of their accumulated retirement savings. According to the Alexander Forbes Member Insights™ for 2021, only 9% of members preserve their retirement savings when changing jobs. This in turn leads to very poor retirement outcomes as the average replacement ratio is only 31%. This means that for every R1 000 earned by a member before retirement, they will only replace R310 of income in their retirement.

Although there will be access allowed to the savings pot in the new system, this is limited to one-third of the individual’s total retirement savings. The other two-thirds must remain preserved at all times.

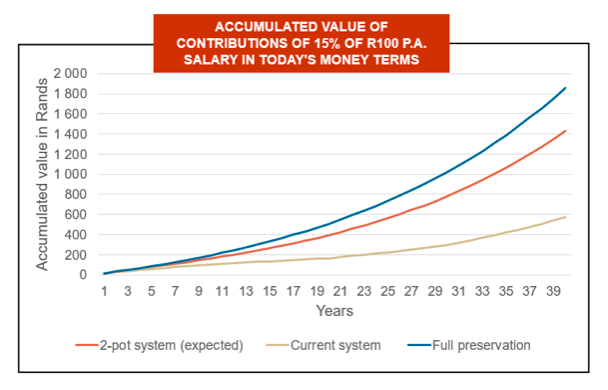

Our modelling has demonstrated that the “two-pot” system will result in a new member accumulating more than double their fund value at retirement as compared to the current system whilst providing access to a portion of their savings annually.

Improving savings – some additional thoughts

While the two-pot proposals go some way to address the issue of preservation, at least in respect of contributions made after 1 March 2023, there are other factors that need to be considered to improve retirement savings:

1. Increasing contributions: At present, the average contribution rate of 12.9%1 (after costs and risk benefits) by members of retirement funds is generally insufficient to achieve the ideal 75% income replacement at retirement.

2. Levels of debt: There is a direct link between the amount of debt individuals have and what they can afford in terms of contributions. In 2021, the Alexforbes Member InsightsTM showed that the debt-to-income ratio of the members was 69%, with 6% of members at high risk of financial stress. “Millennials” in particular, had higher financial stress. The higher the levels of debt and financial stress, the lower the amounts saved toward retirement. This means that to increase retirement savings, interventions are required to assist individuals to live within their means, and budget, reduce their levels of debt and ensure healthy financial habits. More emphasis needs to be put on programmes that assist in doing so.

3. Coverage: Most formally employed individuals are adequately covered, belonging to a formal retirement arrangement. However, there are groups of individuals that are not covered by any form of retirement savings, and it is for these groups that solutions are required as follows:

a. Auto-enrolment for formally employed and contractual workers.

b. Scrapping the means test for the State Old Age Pension at retirement. This acts as a disincentive to save at present.

c. Separate interventions should be thoroughly explored for the informal sector, taking the specific dynamics of this sector into account to ensure a sustainable and workable solution rather than destabilising the integrity of the existing retirement funding system. Many other countries have also grappled with coverage in relation to the informal sector – with limited success in practice.

Overall, Alexforbes is supportive of the changes given that over the long-term the outcomes of retirement members are much improved. In the short-term, however, there will be pressure on administrators to process significant amounts of small claims given that a portion of accumulated savings to 1 March 2024 will be immediately accessible.

It is therefore imperative that retirement funds ensure that they can accommodate the changes including:

– Significant changes to systems making use of the latest technology in engaging members

– Investment strategies to cater for the various pots

– Member communication and support to members to ensure members understand their options under the new system

A further implication may be that free-standing funds consider moving to umbrella funds which would cater for the changes.